Many people know they should buy life insurance “someday”. The real question is when. After marriage? After children? After buying a home?

In reality, waiting too long can make life insurance more expensive—and sometimes harder to get. This guide explains when to consider buying life cover, why starting early helps, and how to choose the right type and amount.

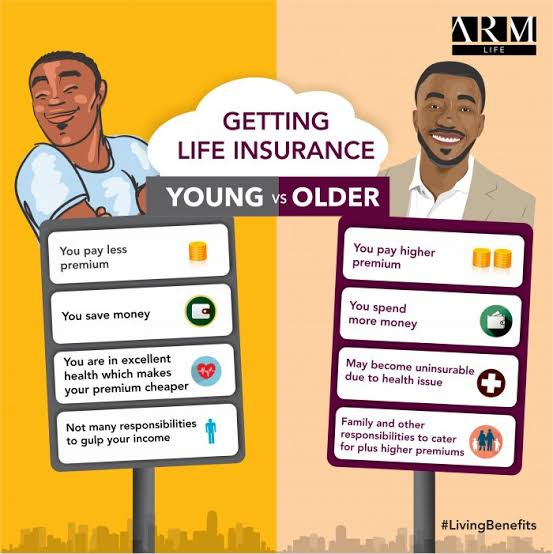

Why Timing Matters When Buying Life Insurance

Life insurance protects your loved ones if your income suddenly stops due to death. Timing matters because two key factors work against you over time:

- Age – Premiums usually increase as you get older.

- Health – Health issues tend to appear with age, which can raise premiums or limit your options.

Buying earlier, when you are younger and healthier, often means:

- More economical premiums

- Better chance of approval

- Access to higher coverage amounts if needed

When Should You Consider Buying Life Insurance?

There is no single “perfect” age, but there are clear life moments when life insurance becomes important:

- You have dependants

- A spouse, children, or parents who rely on your income.

- You have long‑term financial commitments

- Rent or mortgage, car finance, personal loans, business loans.

- You are getting married or starting a family

- You are now responsible for another person’s financial wellbeing.

- You are an expat supporting family abroad

- Your income in the UAE or elsewhere may be critical for relatives back home.

If any of these apply, it is a strong signal that it is time to buy life insurance.

Common Reasons People Delay Buying Life Insurance

People often delay for reasons like:

- “I am still young; I will do it later.”

- “I do not understand the products; it feels complicated.”

- “I have other priorities now—loans, school fees, daily costs.”

- “I get some cover from my employer.”

The problem is that life does not wait. If health changes or something unexpected happens, it may be too late to get the cover you would have wanted—or it may cost much more.

Why Starting Early Can Make a Difference

Starting early can change your life insurance experience in several ways:

- Lower premiums

- Younger and healthier applicants usually pay less for the same coverage.

- More options

- Insurers are more willing to offer a range of products and higher sums assured.

- Longer protection for the same term

- A 25‑year policy bought at 30 protects you until 55; waiting until 40 protects you only to 65 for the same term or costs more if you extend further.

- Peace of mind while you build savings

- Early life insurance gives protection even when your savings are still small.

In short: the earlier you buy, the more value and flexibility you generally get.

How Much Life Insurance Might You Need?

A simple way to estimate your cover is:

- Start with 10–15 times your annual income, then adjust for:

- Outstanding loans and credit

- Children’s school and university costs

- Monthly living expenses for your family

- Any support you send to relatives abroad

Think of your life insurance as a replacement fund for your income. If you are unsure, you can start with a practical amount that fits your budget and review it every few years.

Choosing the Right Type of Life Insurance

Broadly, there are two main types:

- Term Life Insurance

- Covers you for a fixed period (e.g., 10, 20, 25 years).

- Pure protection: no savings or cash value.

- Usually the most economical option for families and main earners.

- Whole of Life / Long‑Term Plans

- Designed to cover you for life or to a high age.

- Some may include savings or investment elements.

- More expensive than term life for the same coverage.

For most people buying life insurance for income and family protection, term life is the natural starting point. More complex plans can be added later if needed and affordable.

Tips for Choosing the Right Life Insurance

When you are ready to buy life insurance, keep these tips in mind:

- Focus on needs, not product names

- First decide what you want to protect (income, debts, education), then match a policy to that goal.

- Be realistic about budget

- It is better to have a slightly smaller policy you can keep paying than a large one that lapses.

- Check what you already have

- Employer cover, bank‑linked cover, or policies from your home country—then decide if it is enough.

- Disclose honestly

- Always be accurate about your health, smoking status, and lifestyle to avoid issues at claim time.

- Review regularly

- Reassess your cover after major changes: new child, job change, new loan, or moving country.

Let Alfred help you compare life insurance options in minutes so you can see how different coverage levels and terms affect your premium.

Conclusion

There will always be reasons to wait, but when it comes to buying life insurance, waiting usually costs more and sometimes closes doors. The best time to buy is when someone depends on your income—or even just before that.

By starting early, choosing the right type of cover, and setting a sensible amount, you can protect your family’s future at a cost that fits your budget today.

Call Instant Alfred to understand your options, and let Alfred help you compare life insurance so you can secure the most economical and effective protection—before life forces you to wish you had done it sooner.